22 / 284

22 / 284

Axiata Group Berhad | Annual Report 2016

MANAGEMENT DISCUSSION & ANALYSIS

020

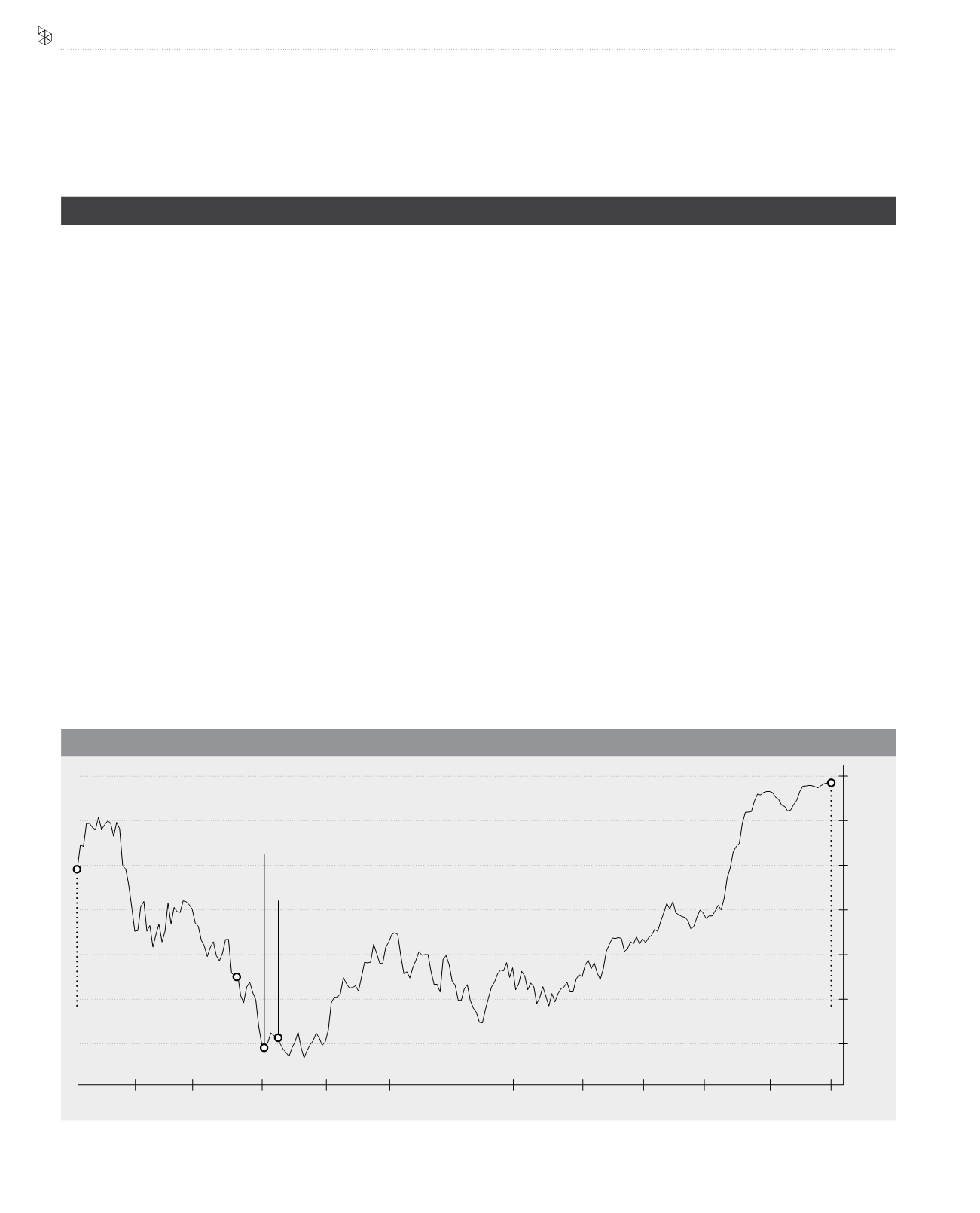

Jan

Start of Year Exchange Rate:

4.2920

End of Year Exchange Rate:

4.4862

March 2016:

Sukuk Drawdown

March 2016:

Loan Drawdown

April 2016:

Ncell Acquisition

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

3.900

4.000

4.100

4.200

4.300

4.400

4.500

2016 IN REVIEW: GROUP PERFORMANCE

GROUP FINANCIAL ANALYSIS 2016

In 2016, Axiata faced challenges from both external events and internal operational weaknesses. Despite this, the Group registered its highest revenue to

date and surpassed the RM20 billion mark for the first time. During the year, Axiata also acquired a new mobile operations, Ncell in Nepal and completed the

first telecommunications merger in Bangladesh with the merger of Robi and Airtel. By end of 2016, both companies were integrated into the Group. The year

concluded with the Group's subscribers growing 16.4% Year on Year (YoY) to approximately 320 million.

Group Performance

The Group saw a revenue growth of 8.5% YoY to reach RM21.6 billion. This was mainly driven by higher revenue recorded by Dialog, Smart and Robi, as well

as contribution from Ncell. The fluctuation of the Ringgit Malaysia against all regional foreign currencies during the year had favourably affected the Group’s

translated revenue.

Data continues to see positive traction and drive growth in revenue with 34.7% increase YoY contributing to 29.2% of total Group revenue, a marked

increase of 5.7 percentage points (pp) from 23.5% in 2015, demonstrating that the Group-wide targeted data investment is paying off. This growth dynamic

is expected to continue at a faster pace for the coming years and will drive the future strategic investment of the Group. Mobile Voice services contributed

45.9% to total Group revenue, a marginal increase of 1.7 pp from the prior year.

The Group achieved double-digit growth in its Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA), increasing 10.0% to RM8.0 billion with

margin improving by 0.6 pp to 37.2%. The increase was mainly due to better contribution from Dialog, XL and Smart. Further to this, the completion of the

acquisition and consolidation of Ncell had contributed RM1.0 billion to the EBITDA of the Group.

The Group’s Profit After Tax and Minority Interest (PATAMI) for the year was RM504.3 million, a decrease of 80.3% YoY. This was attributed to three significant

factors; i) unprecedented external events ii) strategic investments for long-term growth including mergers and acquisitions (M&A) related costs which were

mostly one-offs and iii) underperformance of some OpCos and Associates.

In 2016, Ringgit Malaysia depreciated substantially against all regional foreign currencies and the US Dollar, which had negatively impacted the Group’s profits,

primarily due to US Dollar borrowings for the acquisition of Ncell. Despite disciplined management practices and effectively hedging almost 50% of US Dollar

exposed debt under stringent and forex controlled conditions, the fall of the Ringgit Malaysia against the US Dollar at about 14% during the year, led to net

forex losses of RM685.1 million.

FOREIGN EXCHANGE MOVEMENT OF USD AGAINST RM FROM JANUARY TO DECEMBER 2016

Source : Bloomberg